The Importance of S Corporation Basis and Distribution Elections

S corporations can provide tax advantages over C corporations in the right circumstances. This is true if you expect that the business will incur losses in its early years because shareholders in a C corporation generally get no tax benefit from such losses. Conversely, as an S corporation shareholder, you can deduct your percentage share of these losses on your personal tax return to the extent of your basis in the stock and any loans you personally make to the entity.

Losses that can’t be deducted because they exceed your basis are carried forward and can be deducted by you when there’s sufficient basis.

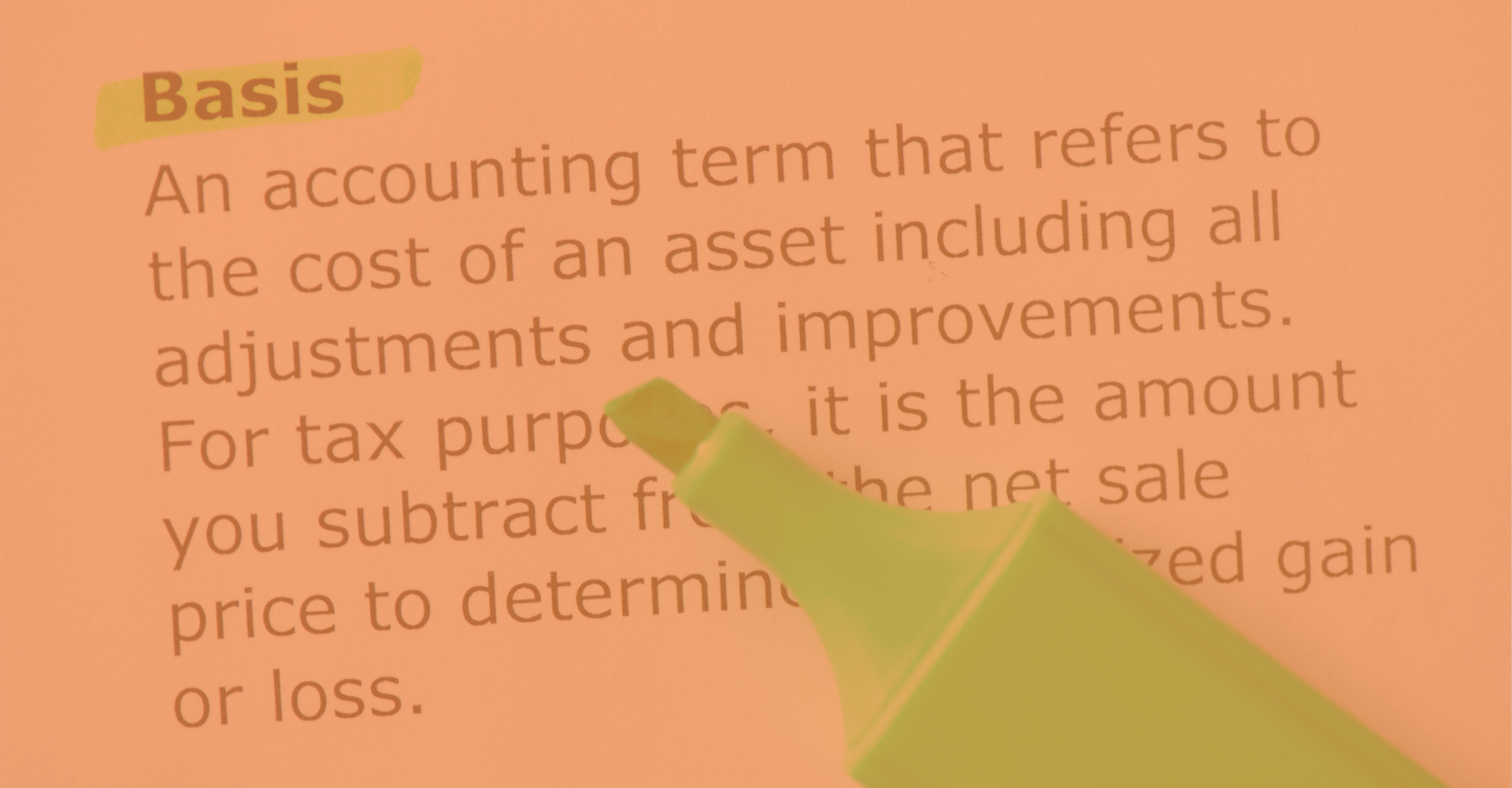

Therefore, your ability to use losses that pass through from an S corporation depends on your basis in the corporation’s stock and debt. And, basis is important for other purposes such as determining the amount of gain or loss you recognize if you sell the stock. Your basis in the corporation is adjusted to reflect various events such as distributions from the corporation, contributions you make to the corporation and the corporation’s income or loss.

Adjustments to basis

However, you may not be aware that several elections are available to an S corporation or its shareholders that can affect the basis adjustments caused by distributions and other events. Here is some information about four elections:

An S corporation shareholder may elect to reverse the normal order of basis reductions and have the corporation’s deductible losses reduce basis before basis is reduced by nondeductible, noncapital expenses. Making this election may permit the shareholder to deduct more pass-through losses.

An election that can help eliminate the corporation’s accumulated earnings and profits from C corporation years is the “deemed dividend election.” This election can be useful if the corporation isn’t able to, or doesn’t want to, make an actual dividend distribution.

If a shareholder’s interest in the corporation terminates during the year, the corporation and all affected shareholders can agree to elect to treat the corporation’s tax year as having closed on the date the shareholder’s interest terminated. This election affords flexibility in the allocation of the corporation’s income or loss to the shareholders and it may affect the category of accumulated income out of which a distribution is made.

An election to terminate the S corporation’s tax year may also be available if there has been a disposition by a shareholder of 20% or more of the corporation’s stock within a 30-day period.